Zusammenfassung. Anthropic und OpenAI haben ihren Distributionskanal für die KI-Produktivitätswelle gewählt: McKinsey, BCG, Bain, Accenture, Goldman Sachs, Blackstone. Zwei Joint Ventures, sechzehn Milliarden Dollar committed, Zielgruppe ein paar tausend Großkunden weltweit. Dieser Kanal wird die 3,44 Millionen Firmen des deutschen Mittelstands nicht erreichen. Der Engpass sind nicht Modelle oder Compute. Der Engpass sind senior Engineers, die bereit und fähig sind, sich in Kundenunternehmen einzubetten und die KI-Fähigkeit in deren Workflows zu integrieren. Ein neues Tier von Boutique-Implementierern formiert sich, um die Lücke zu füllen. Die 51 Prozent der Mid-Market-Firmen, die bereits KI nutzen oder testen (KI-Mittelstandsindex 2026), werden von diesem Tier kaufen, nicht von den Frontier-Lab-Joint-Ventures.

Drei strukturelle Tatsachen und eine Implikation. KI-Produktivität steigt scharf in den USA, mäßig in der EU, kaum in Deutschland. Die Frontier-Labs haben einen Enterprise-Distributionskanal gewählt, der am Mittelstand vorbeiläuft. Der Engpass für alle außerhalb dieses Kanals ist menschlich, nicht technisch. Daher: Die Beratungsbranche teilt sich. Die Mitte verdichtet sich. Ein neues Boutique-Implementierungs-Tier entsteht global, und der Mittelstand wird von diesem Tier kaufen oder gar nicht.

Die Produktivitätsdivergenz ist real

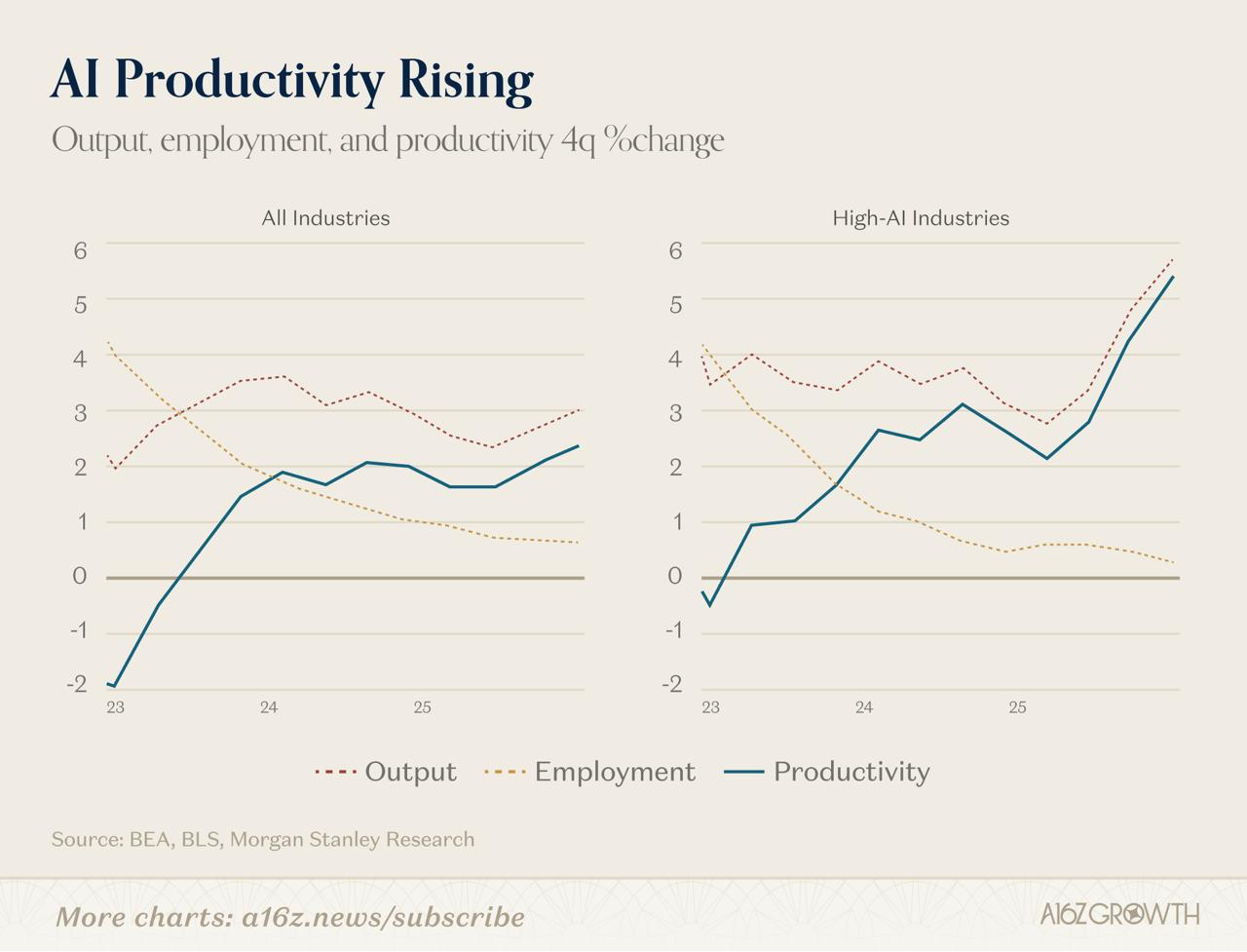

Die a16z-Grafik dieser Woche, basierend auf Morgan-Stanley-Research, zeigt: US-amerikanische Output-pro-Mitarbeiter-Werte schwingen in High-AI-Industries innerhalb von vierundzwanzig Monaten von minus 0,5 Prozent auf plus 5,5 Prozent. Output wächst, während das Beschäftigungswachstum kollabiert, und die Differenz erscheint als Produktivität.

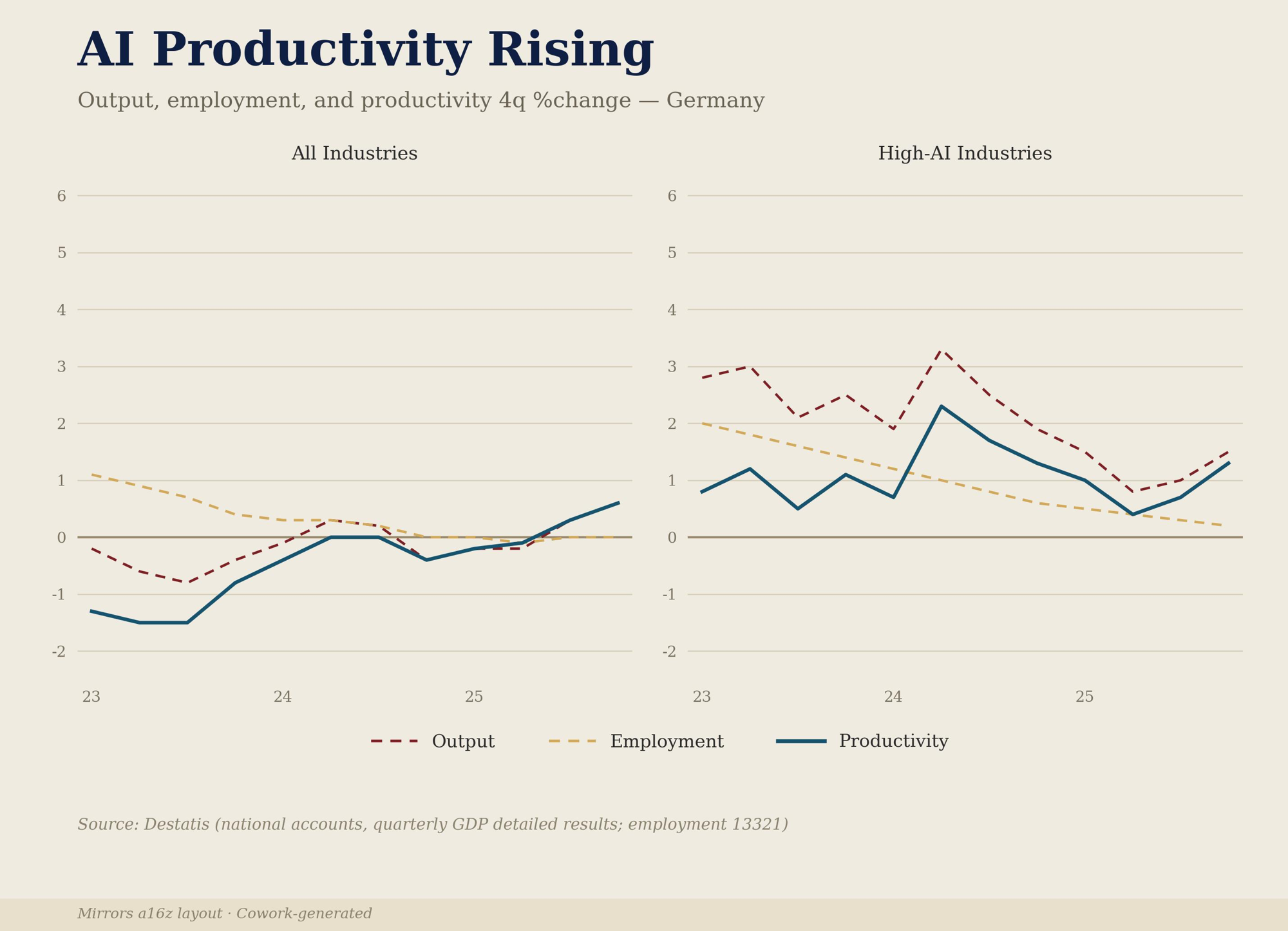

Dieselben Achsen für Deutschland geplottet zeigen die umgekehrte Bewegung. Die deutsche High-AI-Produktivität dezeleriert von +3,3 Prozent in 24Q2 auf etwa +1,5 Prozent bis 25Q4. Der All-Industries-Wert überspringt die Nulllinie spät und nur auf +0,6 Prozent. Die Bitkom-Studie 2026 erklärt den Mechanismus: 41 Prozent aller deutschen Firmen nutzen jetzt KI, aber das KMU-Segment hinkt der größeren Kohorte hinterher, und 53 Prozent aller Befragten nennen „fehlende Kompetenz" als die größte einzelne Hürde für die Adoption. Das ist die Lücke, in der Deutschland lebt: nicht null, aber sichtbar hinter dem europäischen Median und mehrere Größenordnungen hinter den USA.

Die Frontier-Labs haben ihren Distributionskanal gewählt

Im Februar 2026 hat OpenAI die Frontier Alliances mit BCG, McKinsey, Accenture und Capgemini gelauncht: mehrjährige Partnerschaften, in denen OpenAIs eigene Engineers gemeinsam mit Beratungsteams inside Enterprise-Kunden arbeiten.

Im Mai gingen beide Labs einen Schritt weiter. Anthropic hat ein Joint Venture mit Blackstone, Hellman & Friedman, Goldman Sachs und dem singapurischen Staatsfonds GIC angekündigt, kapitalisiert mit rund 1,5 Milliarden Dollar (Anthropic Press Release, 4. Mai 2026). Das Ziel laut Pressemitteilung: Community Banks, mittelgroße Hersteller, regionale Krankenhausverbünde mit fünfzig Millionen bis einer Milliarde Dollar Umsatz. Eine Woche später launchte OpenAI die Deployment Company mit einer Post-Money-Bewertung von 14 Milliarden Dollar (TechCrunch, 11. Mai 2026), gestützt von neunzehn Private-Equity- und Beratungsfirmen, gestartet mit rund 150 senior Engineers ab Tag eins, eingebettet bei Kunden.

Beide Labs spielen das Palantir-Playbook: senior Engineers in die Kundenumgebung schicken, die KI-Plattform an die spezifischen Workflows des Kunden konfigurieren, Account für Account Switching Costs aufbauen. Der Kanal ist gewählt. Er zeigt auf den oberen Mid-Market, die Upper-Mid-Cap und die größten Unternehmen auf der angloamerikanischen Achse.

Er zeigt nicht auf den deutschen Mittelstand.

Der Engpass sind Engineers in Kundenunternehmen, nicht Modelle

Wenn man aufschreibt, was einer dieser eingebetteten Engineers tatsächlich tut, wird das Angebotsproblem offensichtlich. OpenAIs neue Deployment Company startet mit 150 davon weltweit. McKinseys QuantumBlack, BCG X, Deloittes KI-Praxis und Accentures KI-Group erweitern den Pool, aber keine öffentliche Schätzung beziffert die globale Gesamtzahl wirklich senior Implementierer auf mehr als ein paar tausend.

Vergleichen Sie das mit dem deutschen Mittelstand. Das Institut für Mittelstandsforschung (IfM Bonn) zählt 3,44 Millionen deutsche Unternehmen, 99,2 Prozent aller umsatzsteuerpflichtigen Firmen. Neunzehn Millionen Menschen arbeiten dort. Wenn die neuen Frontier-Lab-Joint-Ventures kollektiv 5.000 senior Implementierer für Deutschland über die nächsten zwei Jahre allokieren (eine großzügige Schätzung angesichts der globalen Kopfzahl), ist das Verhältnis ein Implementierer pro 688 Mittelstandsfirmen. Diese 5.000 werden zu den Top-Tausend-Unternehmen nach Umsatz gravitieren. Die verbleibenden 3,43 Millionen sind nicht auf einem Slide-Deck in San Francisco.

Die Nachfrage liegt vier bis sechs Größenordnungen höher als dieses Angebot.

Ein neues Tier formiert sich

Während die Frontier-Labs ihre Beratungs-Joint-Ventures bauten, formierte sich auf dem offenen Markt ein paralleles Tier. Kleine, technisch tiefe, Builder-first Firmen, besetzt mit senior Engineers, die KI direkt in Kundenumgebungen konfigurieren. Anders als Big Consulting. Anders als generische Software-Anbieter. Anders als Staff Augmentation. Die klarsten Beispiele sind aktuell amerikanisch.

Tenex.co verkauft „AI Transformation und AI Engineering Squads", Zielgruppe Enterprises mit organisationsweiter KI-Strategie. Alephic bettet Engineers in Marketing-Organisationen bei Amazon, Meta, PayPal, Ford, Disney und EY ein. Slogan: „Builders, not consultants. We solve problems by shipping code, not PowerPoints." Distyl AI hat dasselbe Modell zur milliardenschweren Firma skaliert, mit outcome-based Pricing für Fortune-500-Kunden in Healthcare, Telekommunikation, Versicherung, Fertigung und Finanzdienstleistung. Patterns AI, gegründet von Ex-Anthropic-Engineers, sitzt im gleichen Tier. Every kombiniert einen KI-nativen Newsletter mit Beratungsdiensten und eigenen ausgelieferten Softwareprodukten, positioniert sich als „AI training, adoption and innovation, from makers, not management consultants".

Keine dieser Firmen sieht aus wie McKinsey. Keine versucht es. Sie verkaufen tiefe technische Fluency, schnelle Liefer-Zyklen und die Bereitschaft, Engineers direkt neben die eigenen Leute des Kunden zu stellen. Das Muster ist über alle hinweg erkennbar.

Dieses Tier existiert auch in Deutschland, in früherer und kleinerer Form, explizit auf Mittelstand-Kunden und EU-AI-Act-Compliance fokussiert. Die Kombination aus Frontier-Lab-Supply-Konzentration plus dem regulatorischen Stichtag August 2026 (High-Risk-Verpflichtungen unter dem EU AI Act gehen live) bedeutet: das deutsche Tier wird entweder schnell expandieren oder das Feld internationalen Firmen überlassen, die zu spät kommen.

Wie Sie einen echten Implementierungspartner erkennen

Die Bitkom-Studie 2026 nennt die drei größten Hürden für die KI-Adoption in deutschen Firmen: fehlende Kompetenz (53 Prozent), Datenschutz (44 Prozent) und Integration in bestehende Prozesse (39 Prozent). Ein echter Implementierungspartner muss diese drei beim Erstkontakt auflösen. Drei Marker, die sich im Erstgespräch prüfen lassen.

Versteht er Ihr Geschäft? Kann der Partner Ihre Branche, Ihr Operating Model und den spezifischen Workflow, den er verändern will, in der Sprache Ihrer Operatoren beschreiben, vor dem zweiten Meeting? Generische „KI-Strategie"-Decks sind der Failure-Mode. Partner, die keinen Use Case innerhalb einer Stunde auf Ihre P&L abbilden können, überleben den Kontakt mit einer realen Produktionsumgebung nicht.

Schult er Ihr Team? Die Schulung der eigenen Leute ist laut Bitkom der größte einzelne Hebel für Adoption-Erfolg. Ein Partner, der ein funktionierendes System liefert, aber keine interne Capability hinterlässt, ist eine One-Shot-Ausgabe, keine Transformation. Frage: Wie bauen Sie interne Capacity auf, wie sieht die Übergabe aus, wie sieht die Organisation Ihres Kunden sechs Monate nach Ihrem Abgang aus?

Kann er Compliance? EU-AI-Act Artikel-5-Verbote sind seit Februar 2025 live. High-Risk-Verpflichtungen folgen im August 2026. DSGVO ist permanent. Ein Partner, der die spezifischen Regulierungs-Artefakte, die für Ihren Use Case gelten (AI-Act-Risikoklassifikation, Standard-AVV-Verträge, branchenspezifische Frameworks wo vorhanden), nicht beim Erstkontakt benennen kann, wird zur externen Abhängigkeit in dem Moment, wo ein Regulator nachfragt.

Unter den drei Markern liegt ein universeller Test: Liefert er funktionierende Software in Wochen, nicht Präsentations-Decks in Quartalen? „Builders, not consultants" ist kein Marketing-Spruch. Es ist das einzige Liefermodell, das die Zeit zwischen Board-Approval und operativem Impact auf die Monate komprimiert, in denen Ihre Wettbewerber auch arbeiten.

Was folgt für Founder, Boards und PE

Mittelstands-CEO. Warten Sie nicht, bis ein Anthropic- oder OpenAI-Partner-Programm anruft. Die Montag-Aktion: identifizieren Sie den Implementierungspartner, der die drei Marker oben besteht und einen laufenden Piloten in Produktion bringt, innerhalb von neunzig Tagen. Die Legal Form (unabhängiger Spezialist, Partner-Netzwerk, kleine Boutique) spielt keine Rolle. Die Marker tun es.

Senior AI Implementierer (solo oder Boutique). Zehn-Jahres-Vorlauf, kein Achtzehn-Monats-Trade. Spezialisieren Sie sich auf zwei oder drei Vertikalen, die Sie wirklich verstehen. Dokumentieren Sie Ihre Liefermuster öffentlich. Behandeln Sie Vibe-Coding und rigorose Evaluation als die zwei Hälften des senior Crafts, nicht als gegenüberliegende Lager. Bauen Sie Compliance-Fluency als explizite Service-Line auf, nicht als Fußnote.

Mid-Market-PE-Investor. Klassische Body-Shop-Beratungen im Portfolio mit deutlich niedrigeren Multiples neu unterschreiben. Vertikale Boutiquen und KI-native Implementierungsfirmen mit längeren Halteperioden und höheren Multiples neu unterschreiben. Die Mitte verdichtet sich, die Ränder nicht.

Board eines mittelständischen Industrieunternehmens. Die Frage für die nächste Sitzung ist nicht „sollen wir KI adaptieren", sondern „welche interne KI-Implementierungs-Capacity haben wir, woher kommt sie, wie compoundet sie". Die 43 Prozent Mittelstandsfirmen ohne geschriebene KI-Strategie (BVMW Mittelstand Index 2026) sind die, deren Wettbewerbsposition gerade jetzt still erodiert.

Die Modelle sind verteilbar. Die Engineers nicht. Wer den Mittelstand erreicht, erreicht Deutschland.

Wie ich helfe

Ich betreibe eine kleine Implementierungspraxis aus München. Builder-first, Claude-Code-native, deutsch und englisch, fokussiert auf die drei Bitkom-Hürden oben und den August-2026-AI-Act-Stichtag.

Die Arbeit läuft in drei Schichten, jede für einen anderen Buying-Moment designed.

Diagnose- und Assessment-Formate (unter 1.000 €). Für den CEO, das Board-Mitglied oder den Operator, der einen konkreten Startpunkt in Tagen will, nicht in Wochen. Ein KI-Readiness-Assessment, ein AI-Act-Risiko-Klassifikations-Check, eine Claude-Code-Adoption-Bewertung für ein einzelnes Team. Designed, ohne Procurement-Meeting entscheidbar zu sein.

Fokussierte Engagements (zwischen 1.000 € und 5.000 €). Compliance-Sprints, halbtägige Strategie-Workshops mit dem Leadership-Team, Use-Case-Validierungen gegen Ihre eigenen Daten. Outcome ist ein schriftliches Deliverable plus eine Entscheidung: gehen wir weiter, und wenn ja, woran.

Custom Pilot Engagements (pro Case gescoped). Ein priorisierter Use Case von Discovery zu Produktion innerhalb von neunzig Tagen. Interne Übergabe am Ende, damit Ihr eigenes Team besitzt und betreibt, was wir gebaut haben.

Weitere Low-Barrier-Formate launchen in den kommenden Wochen, während der Entry-Level-Katalog wächst. Der schnellste Weg, heute zu starten, ist ein kostenloser dreißig-minütiger Discovery Call. Keine Verpflichtungen, kein Kalt-Akquise-Follow-up. Buchen unter drfloriansteiner.com.

Leiten Sie dies an einen CEO, ein Board-Mitglied oder einen PE-Partner weiter, der über dieselben Fragen nachdenkt. Abonnieren Sie unter drfloriansteiner.com für den nächste Woche erscheinenden Weekly Agentic Engineering Digest zu KI, Claude Code und dem neuen Vibe-Coding-Implementierungs-Tier.